Quick Answer

In Canada, a buyer earning $80,000, $100,000 or $150,000 may qualify for very different mortgage amounts depending on debt, down payment, credit score, property taxes, condo fees, interest rate and the mortgage stress test.

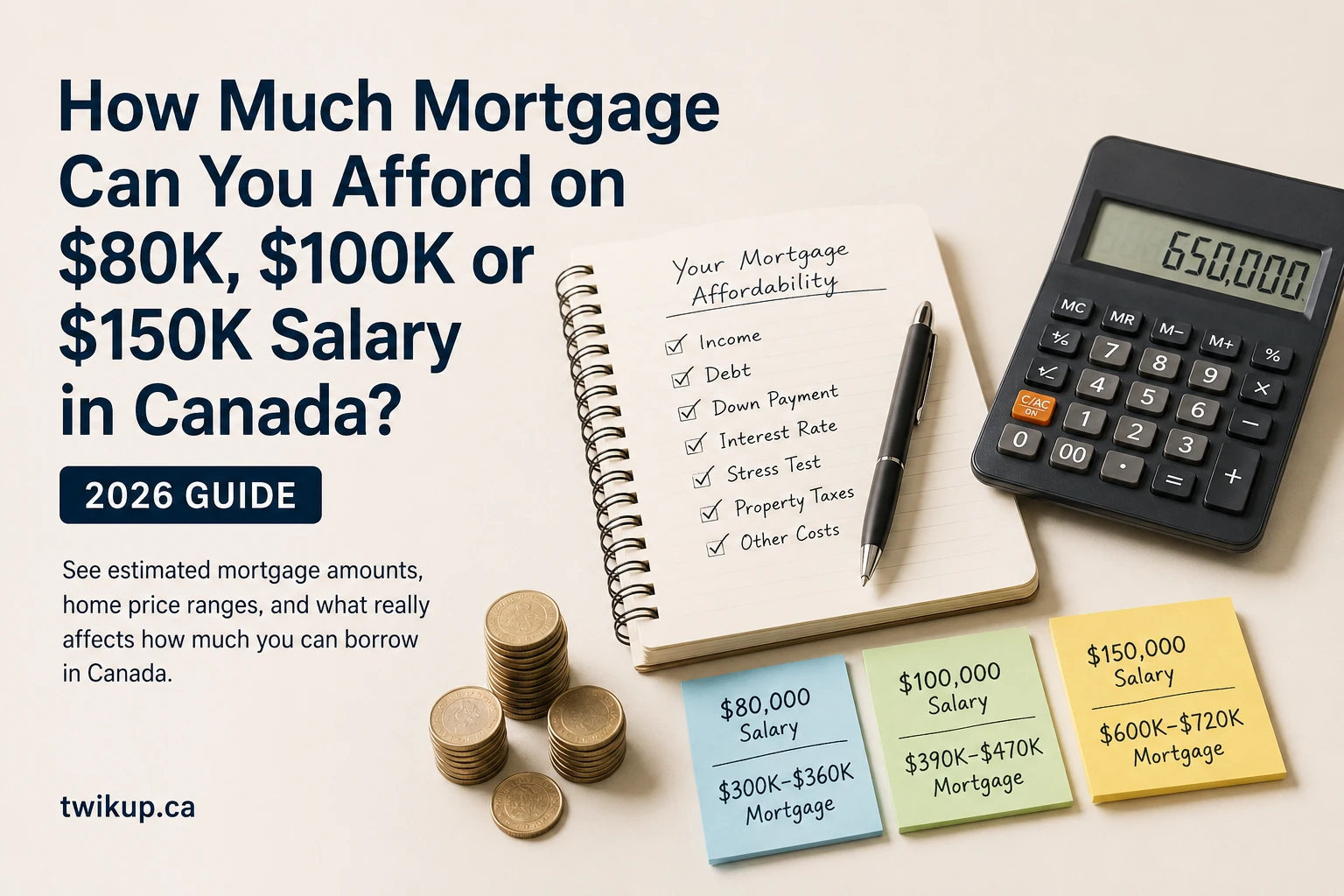

As a rough 2026 estimate:

| Gross Household Income | Estimated Mortgage Range | Estimated Home Price Range |

|---|---|---|

| $80,000 | $300,000–$360,000 | $325,000–$425,000 |

| $100,000 | $390,000–$470,000 | $425,000–$550,000 |

| $150,000 | $600,000–$720,000 | $675,000–$900,000 |

These are educational estimates only. Your actual approval can be higher or lower.

Important 2026 Assumptions

This article assumes:

- You are buying in Canada.

- You have stable employment income.

- You have decent credit.

- You have little or no other debt.

- You are using a 25-year amortization.

- You are being tested under Canadian mortgage stress test rules.

- Property taxes, heating costs and possible condo fees are included.

Canada’s mortgage stress test generally requires borrowers to qualify at the greater of the mortgage contract rate plus 2% or 5.25%, according to OSFI. CMHC also uses debt service ratios such as GDS and TDS when assessing mortgage affordability.

Before You Read: Mortgage Affordability Is Not the Same as Real Affordability

Many buyers ask:

“How much mortgage can I get?”

But the better question is:

“How much mortgage can I comfortably afford without becoming house poor?”

That difference matters.

A bank may approve you for a certain amount, but that does not mean the payment will feel comfortable once you add:

- property tax

- home insurance

- utilities

- maintenance

- car payments

- childcare

- groceries

- emergency savings

- retirement savings

- future rate increases

For a beginner-friendly explanation, read Twikup’s earlier guide: How Much House Can You Really Afford in Canada? Most Buyers Get This Wrong

How Much Mortgage Can I Afford on an $80,000 Salary?

If your household income is $80,000 per year, your gross monthly income is about:

$6,667 per month

Using a 39% housing-cost guideline, your maximum housing-cost room may be around:

$2,600 per month

But that amount does not go entirely toward the mortgage. It must also cover property tax, heating and sometimes condo fees.

Estimated Mortgage on $80,000 Salary

| Scenario | Estimated Mortgage |

|---|---|

| Conservative | $300,000–$325,000 |

| Moderate | $325,000–$350,000 |

| Stretch | $350,000–$360,000+ |

Estimated Home Price on $80,000 Salary

Depending on down payment, a buyer earning $80,000 may look around:

$325,000 to $425,000

In expensive markets like Toronto, Vancouver or parts of the GTA, this may be difficult without a larger down payment, second income or lower debt.

Twikup Insight

On an $80,000 salary, the biggest risk is not only qualifying. The bigger risk is buying so close to the limit that one surprise expense breaks your monthly budget.

A safer approach is to calculate the mortgage payment first, then ask:

“Can I still save money every month after owning this home?”

How Much Mortgage Can I Afford on a $100,000 Salary?

If your household income is $100,000 per year, your gross monthly income is about:

$8,333 per month

Using a 39% housing-cost guideline, your maximum housing-cost room may be around:

$3,250 per month

After property tax, heat and other housing costs, the mortgage payment room may support a larger loan.

Estimated Mortgage on $100,000 Salary

| Scenario | Estimated Mortgage |

|---|---|

| Conservative | $390,000–$420,000 |

| Moderate | $420,000–$450,000 |

| Stretch | $450,000–$470,000+ |

Estimated Home Price on $100,000 Salary

A buyer earning $100,000 may often look around:

$425,000 to $550,000

This may work better in smaller cities, parts of Alberta, Saskatchewan, Manitoba, Atlantic Canada, or more affordable Ontario markets.

Twikup Insight

A $100,000 salary sounds strong, but in Canada’s major housing markets it may still feel tight if you have car loans, student loans, credit card debt or childcare costs.

Before shopping, get pre-approved properly. Read: How to Get Mortgage Pre-Approval in Canada

How Much Mortgage Can I Afford on a $150,000 Salary?

If your household income is $150,000 per year, your gross monthly income is about:

$12,500 per month

Using a 39% housing-cost guideline, your maximum housing-cost room may be around:

$4,875 per month

After property taxes, heat and other housing costs, this may support a significantly larger mortgage.

Estimated Mortgage on $150,000 Salary

| Scenario | Estimated Mortgage |

|---|---|

| Conservative | $600,000–$650,000 |

| Moderate | $650,000–$700,000 |

| Stretch | $700,000–$720,000+ |

Estimated Home Price on $150,000 Salary

A household earning $150,000 may often look around:

$675,000 to $900,000

The final number depends heavily on down payment. A larger down payment can increase the home price without increasing the mortgage amount.

Twikup Insight

At $150,000 income, many buyers make a different mistake: they assume higher income automatically means safety.

But higher-priced homes also bring higher:

- land transfer tax

- property tax

- insurance

- maintenance

- closing costs

- furniture costs

- repair costs

A $150,000 household can still become house poor if the purchase is stretched too far.

Why Two People With the Same Salary May Get Different Mortgage Amounts

Two buyers earning $100,000 can receive very different approvals.

Why?

Because lenders also look at:

- credit score

- existing debt

- down payment

- employment type

- income stability

- property taxes

- condo fees

- heating costs

- amortization

- mortgage rate

- stress test rate

A person earning $100,000 with no debt may qualify for much more than someone earning $100,000 with a $700 car payment and credit card balances.

The Mortgage Stress Test Can Reduce Your Buying Power

The mortgage stress test is one of the biggest reasons buyers qualify for less than expected.

Even if your actual mortgage rate is lower, lenders may test your affordability at a higher qualifying rate. OSFI states the minimum qualifying rate for uninsured mortgages is the greater of the contract rate plus 2% or 5.25%.

Example:

If your mortgage rate is 4.25%, you may need to qualify at:

6.25%

That higher test rate reduces the mortgage amount you can borrow.

For a deeper explanation, read: Mortgage Stress Test Explained

Down Payment Also Changes What You Can Buy

Your mortgage amount and your home price are not the same thing.

Home price = mortgage + down payment

CMHC explains that insured purchases can start with a minimum down payment of 5%, while homes above $500,000 require 5% on the first $500,000 and 10% on the portion above $500,000. Homes $1.5 million or more generally require at least 20% down and are not eligible for CMHC insurance.

For a full breakdown, read: Down Payments in Canada Explained

Simple Rule of Thumb by Salary

| Salary | Safer Mortgage Mindset |

|---|---|

| $80,000 | Focus on payment comfort first |

| $100,000 | Avoid debt before applying |

| $150,000 | Do not confuse approval with affordability |

A rough mortgage range may be:

- $80,000 salary: around 3.75x to 4.5x income

- $100,000 salary: around 4x to 4.7x income

- $150,000 salary: around 4x to 4.8x income

But this rule can break quickly when rates, taxes, debt or condo fees rise.

Example: Why Debt Can Lower Your Mortgage Approval

Suppose two buyers both earn $100,000.

Buyer A

- No car loan

- No credit card debt

- No student loan

- Strong credit

- Good down payment

Buyer A may qualify near the higher end of the range.

Buyer B

- $650 monthly car payment

- $250 student loan payment

- Credit card balance

- Smaller down payment

Buyer B may qualify for much less, even with the same income.

This is why mortgage affordability is not only about salary. It is about total monthly obligations.

Should You Borrow the Maximum Mortgage Amount?

Usually, no.

Borrowing the maximum may make sense mathematically, but it can create emotional and financial pressure.

Before borrowing the maximum, ask:

- Can I handle higher utility bills?

- Can I still save every month?

- Can I afford repairs?

- Can I handle job loss or income reduction?

- Can I manage renewal risk if rates change?

- Will I still have money for life outside the mortgage?

A home should improve your financial life, not trap it.

Twikup Practical Affordability Formula

Instead of starting with the bank’s maximum approval, Twikup suggests this order:

- Decide your comfortable monthly payment.

- Add property tax, heat, insurance and maintenance.

- Subtract existing debts.

- Stress-test your own budget.

- Then get pre-approved.

- Then shop for homes below your maximum.

This keeps the decision buyer-first, not lender-first.

For mortgage basics, read: What Is a Mortgage and How Does It Work in Canada?

Final Answer: How Much Mortgage Can You Afford?

| Income | Estimated Mortgage | Better Buyer Strategy |

|---|---|---|

| $80,000 | $300K–$360K | Stay conservative and protect cash flow |

| $100,000 | $390K–$470K | Reduce debt before applying |

| $150,000 | $600K–$720K | Avoid lifestyle inflation and overbuying |

The best mortgage is not always the biggest mortgage.

The best mortgage is the one you can afford comfortably, even after taxes, repairs, insurance, groceries, savings and future life changes.

Disclaimer

This article is for general educational purposes only and is not mortgage, legal, financial or investment advice. Mortgage approvals depend on lender criteria, credit profile, income verification, debt levels, down payment, property type, location, interest rates and government rules. Always speak with a licensed mortgage professional before making a home-buying decision.