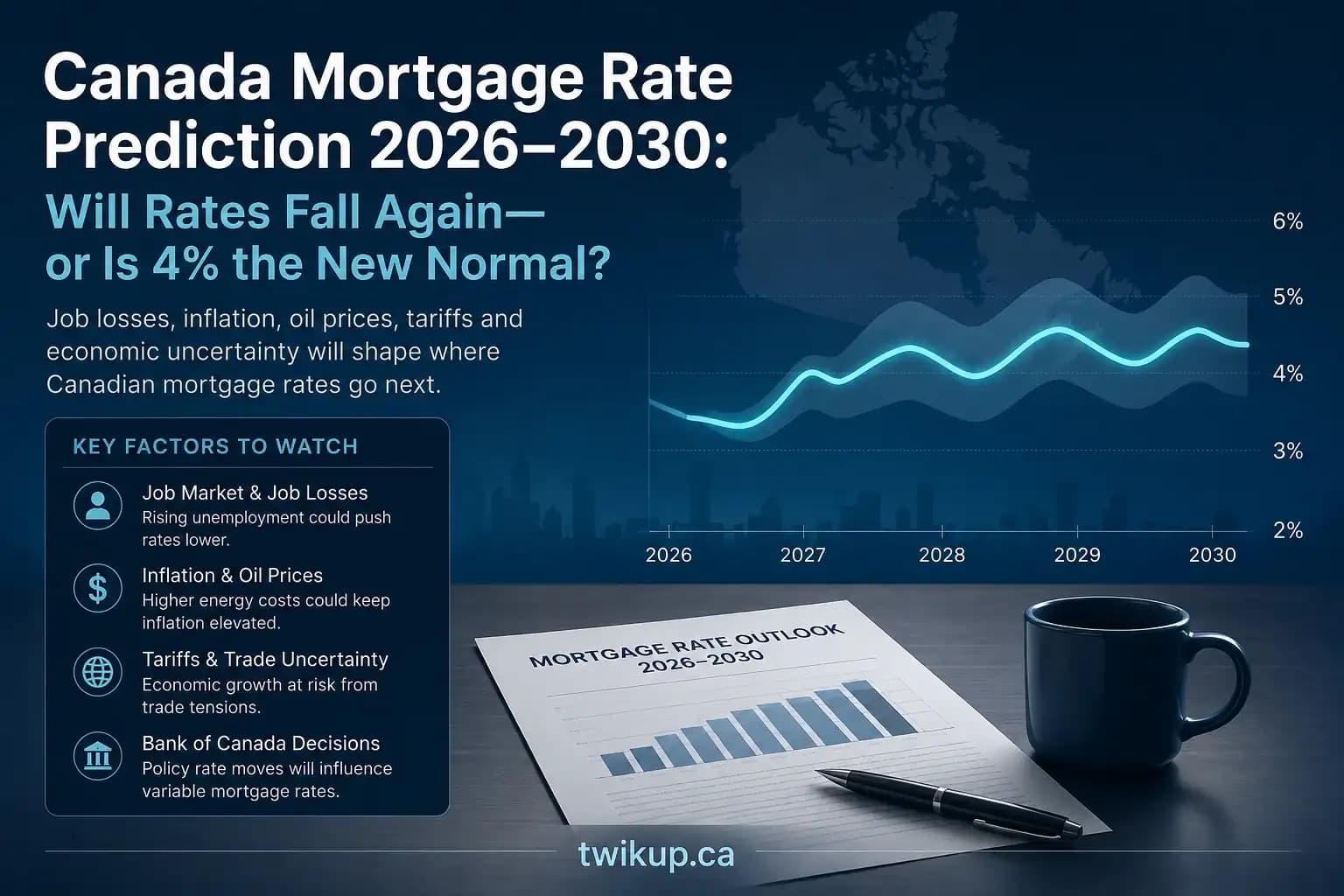

Will Canadian mortgage rates finally fall, or is 4% the new normal? Explore Twikup’s 2026–2030 mortgage rate prediction, including how job losses, inflation, oil prices, tariffs and the Canadian economy could shape fixed and variable mortgage rates over the next five years.

Buying a home as a single parent in Canada can be challenging—but it may be more achievable than you think. Learn how mortgage qualification works, which first-time buyer programs and tax credits may help, and how to determine what you can realistically afford in 2026.

Wondering what the monthly payment is on a $500K, $700K, or $1 million home in Canada? Here's a practical 2026 guide with payment estimates, affordability tips, and the hidden costs buyers often overlook.

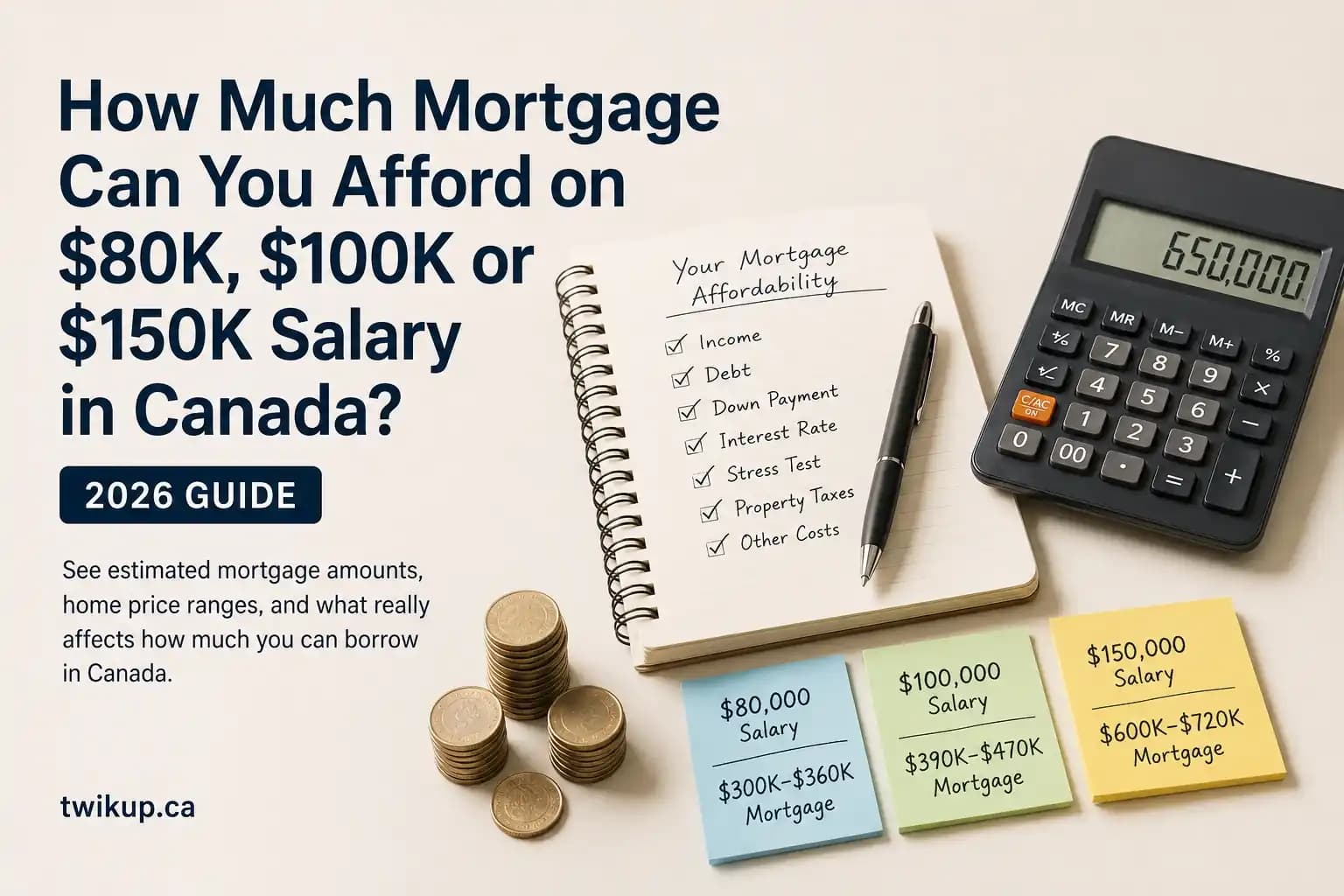

Wondering how much mortgage you can afford on an $80,000, $100,000 or $150,000 salary in Canada? This 2026 guide explains estimated mortgage ranges, home price affordability, the mortgage stress test, down payment impact and why your salary alone doesn't determine how much you can borrow. Learn how lenders assess affordability and avoid becoming house poor before buying your next home.

Wondering how mortgage brokers make money in Canada? Most brokers are paid by lenders—not homebuyers—but there are important exceptions every borrower should understand. Learn how mortgage broker commissions work, when broker fees apply, and how to choose the right mortgage professional for your home purchase in this comprehensive 2026 guid

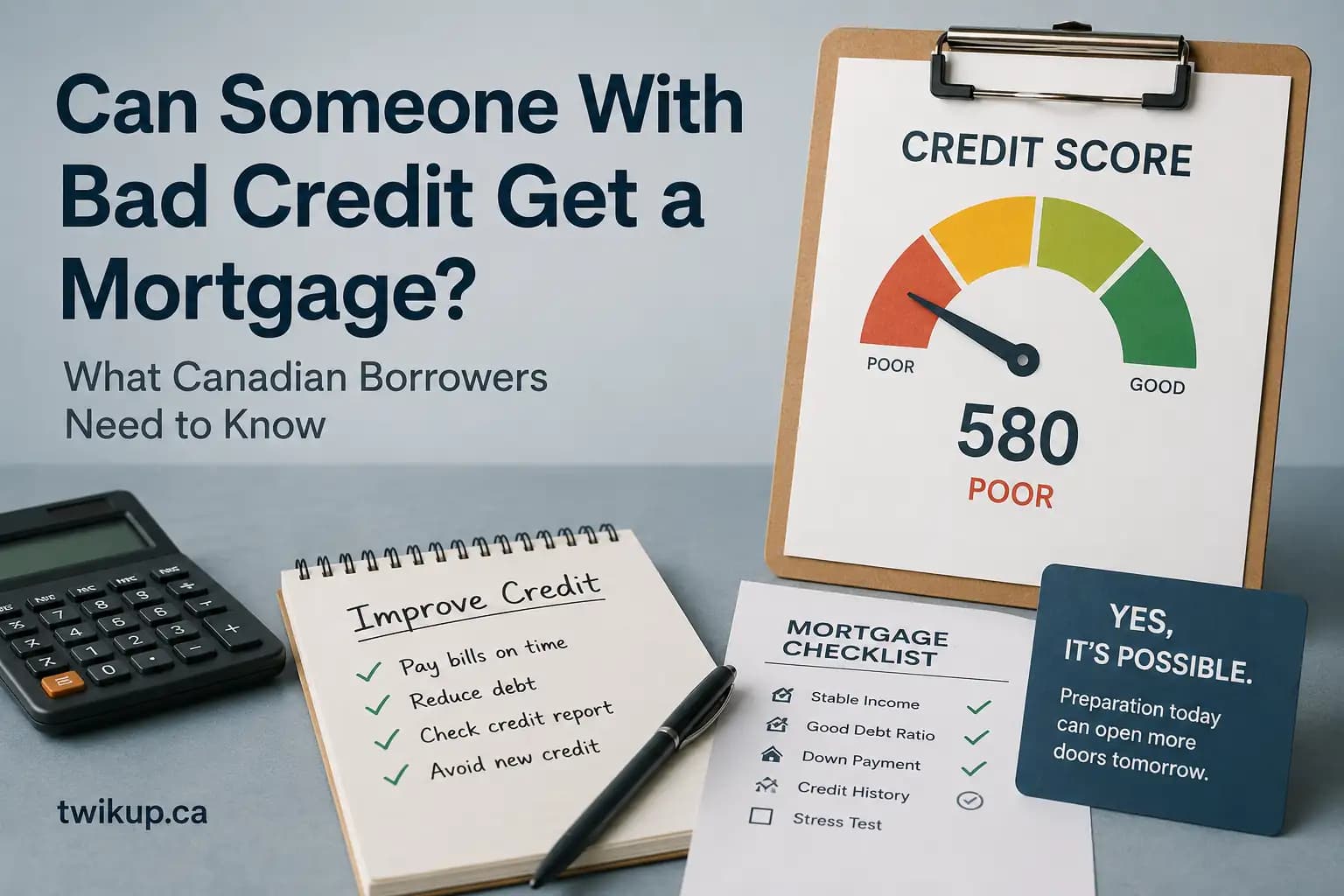

Your credit score can be the difference between getting the best mortgage rate or paying thousands more in interest. In Canada, most lenders prefer a credit score of 680 or higher, but homeownership may still be possible with lower scores. This guide explains the minimum credit score needed for a mortgage in 2026, how lenders evaluate borrowers, and practical ways to improve your approval chances while reducing long-term borrowing costs.

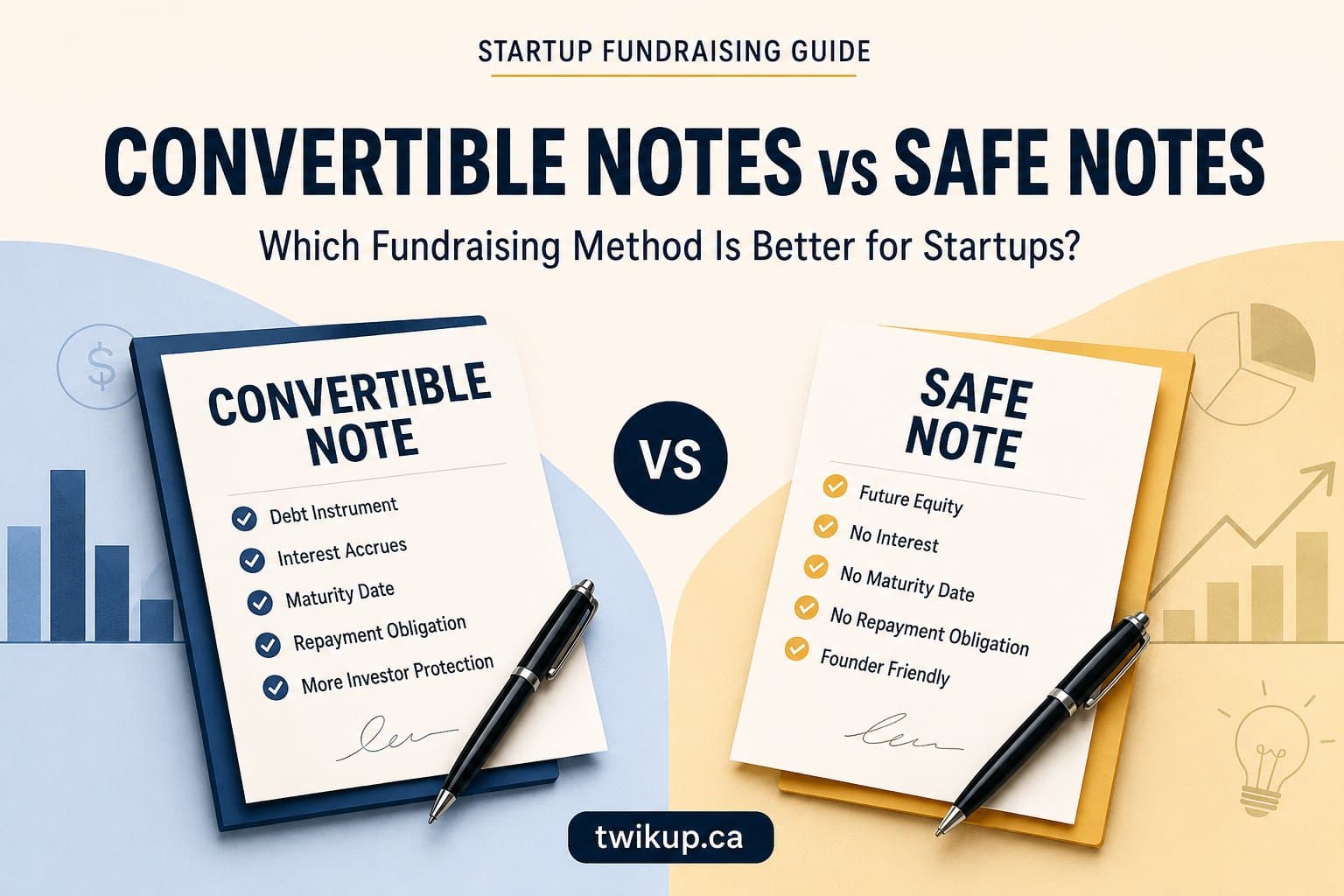

SAFE Notes and Convertible Notes are two of the most common startup fundraising tools, but choosing the wrong one can affect dilution, investor relationships, and future funding rounds. Learn the key differences, advantages, risks, and which option is best for founders in 2026.

Many Canadians focus on mortgage rates, down payments, and pre-approvals, only to discover that the mortgage stress test significantly reduces the amount they can borrow.

This guide explains exactly how Canada's mortgage stress test works in 2026, how lenders calculate qualification, how it impacts affordability, and practical strategies to improve your approval chances.

Many Canadians believe they need a 20% down payment to buy a home—but that's not always true. This guide explains minimum down payment rules in Canada, mortgage insurance, closing costs, common mistakes, and how much money you realistically need before buying your first home.

Mortgage pre-approval is one of the most important steps in the home-buying process, yet many Canadians misunderstand how it works. Learn what lenders look for, how much you can qualify for, how to improve your approval odds, and why pre-approval can save you thousands when buying a home in Canada.

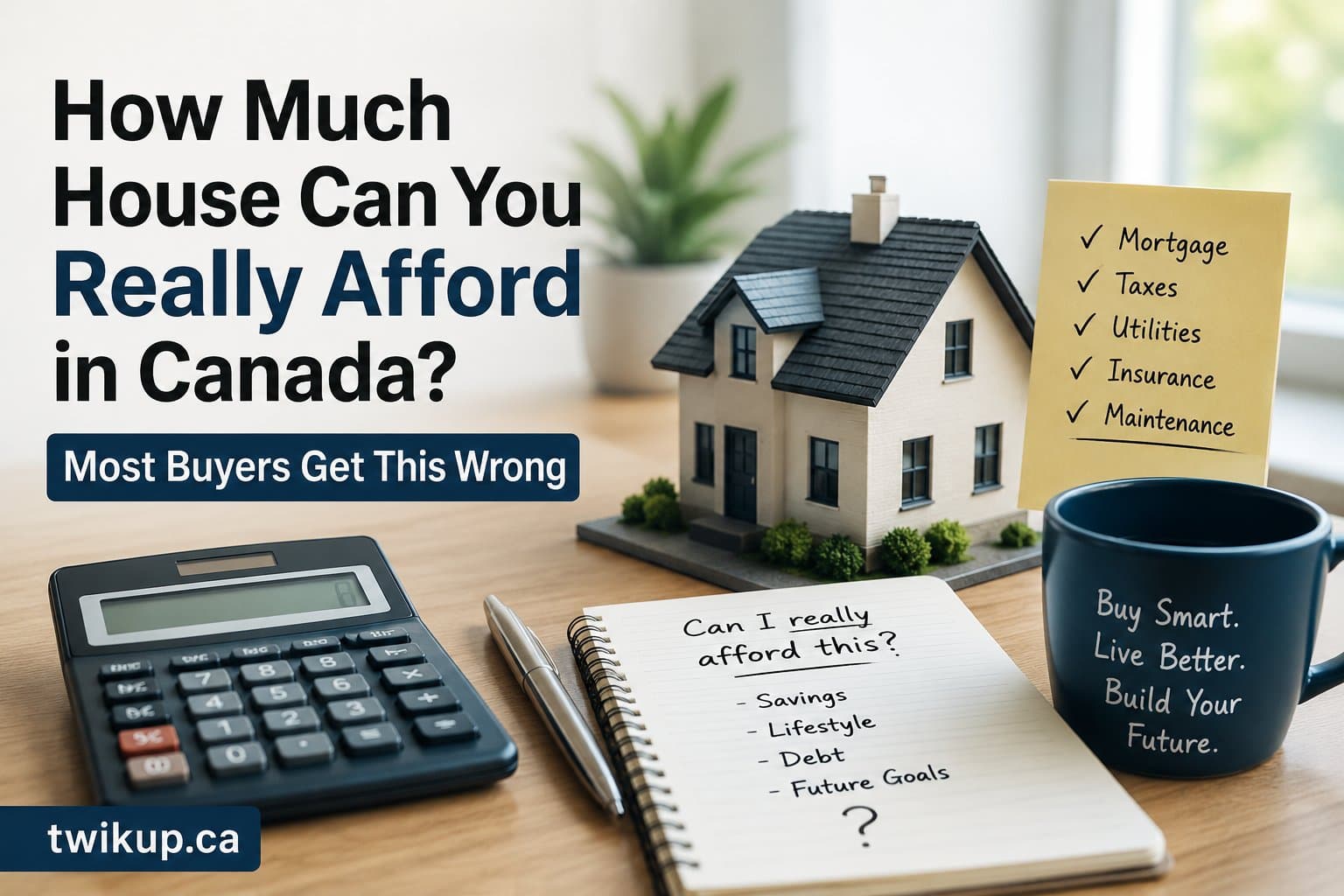

Many Canadians focus on how much mortgage they can qualify for, but qualification and affordability are not the same thing. Learn how to calculate a realistic home-buying budget, avoid becoming house poor, and understand the hidden costs of homeownership in Canada.

A mortgage is one of the biggest financial commitments most Canadians will ever make, yet many buyers do not fully understand how it works. Learn the basics of mortgages, down payments, interest rates, amortization, and mortgage approval in this beginner-friendly Canadian guide from Twikup.

A fixed mortgage offers greater payment certainty in 2026, but lower variable rates could still save money. The real question is what happens if rates rise in 2027.

Canada’s interest rates are expected to remain steady as inflation stays above target. Borrowers approaching mortgage renewal may need to prepare for a prolonged period of higher borrowing costs.

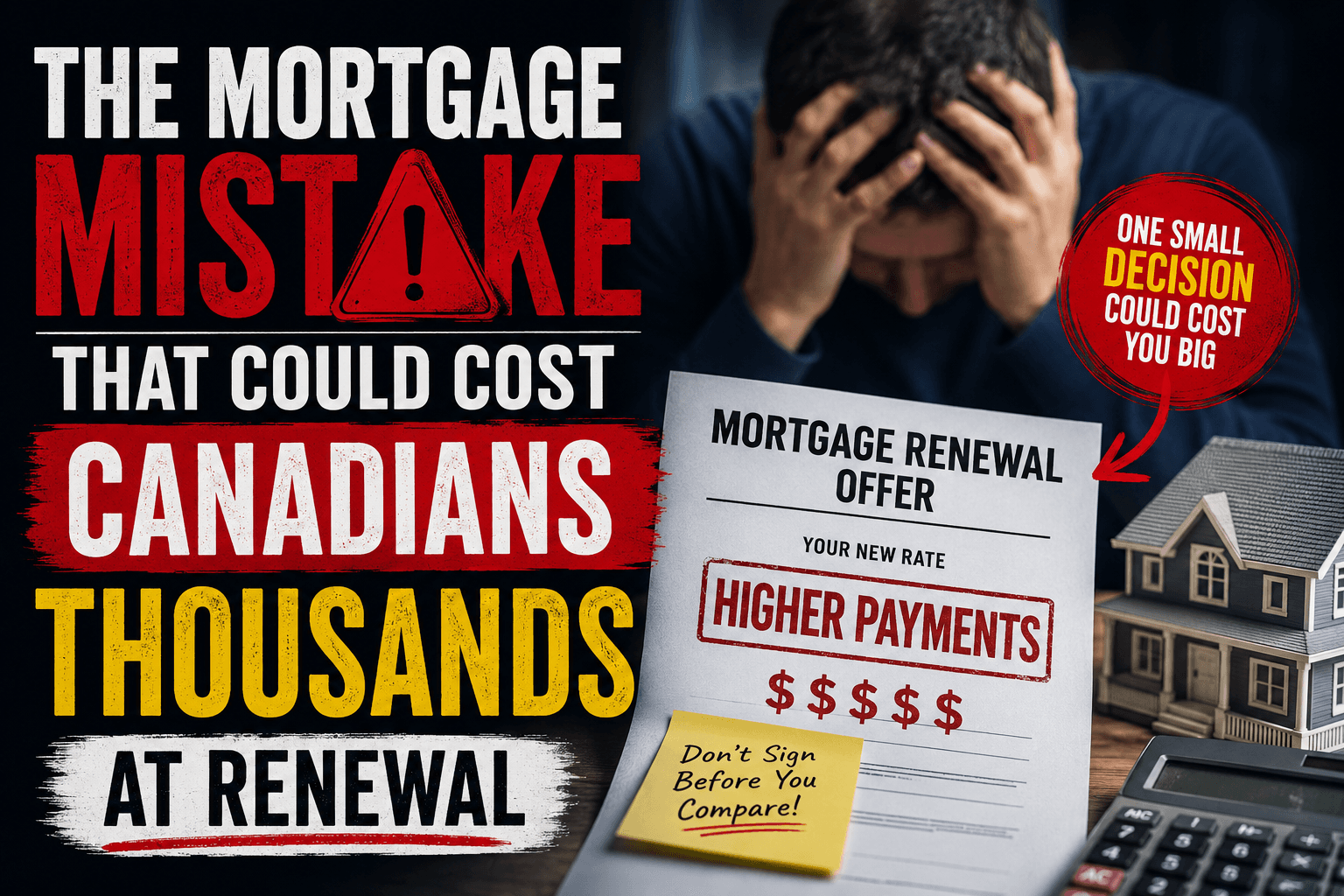

Many Canadians make a costly mistake at mortgage renewal by accepting the first offer from their lender. Experts recommend comparing rates, securing a rate hold, getting written quotes, and negotiating using competing offers. Homeowners should also avoid early-renewal traps and understand switching costs before signing. Even a small difference in mortgage rates can add up to thousands of dollars in extra interest over the next mortgage term.