Many middle-class Canadians work hard, earn respectable incomes, and still feel financially stretched. The reason is often not a lack of earnings but a handful of money habits that quietly consume wealth-building opportunities year after year.

The gap between income and financial security frequently comes down to behavior. Certain habits feel normal in everyday life but can significantly slow progress toward savings, investing, and long-term financial stability.

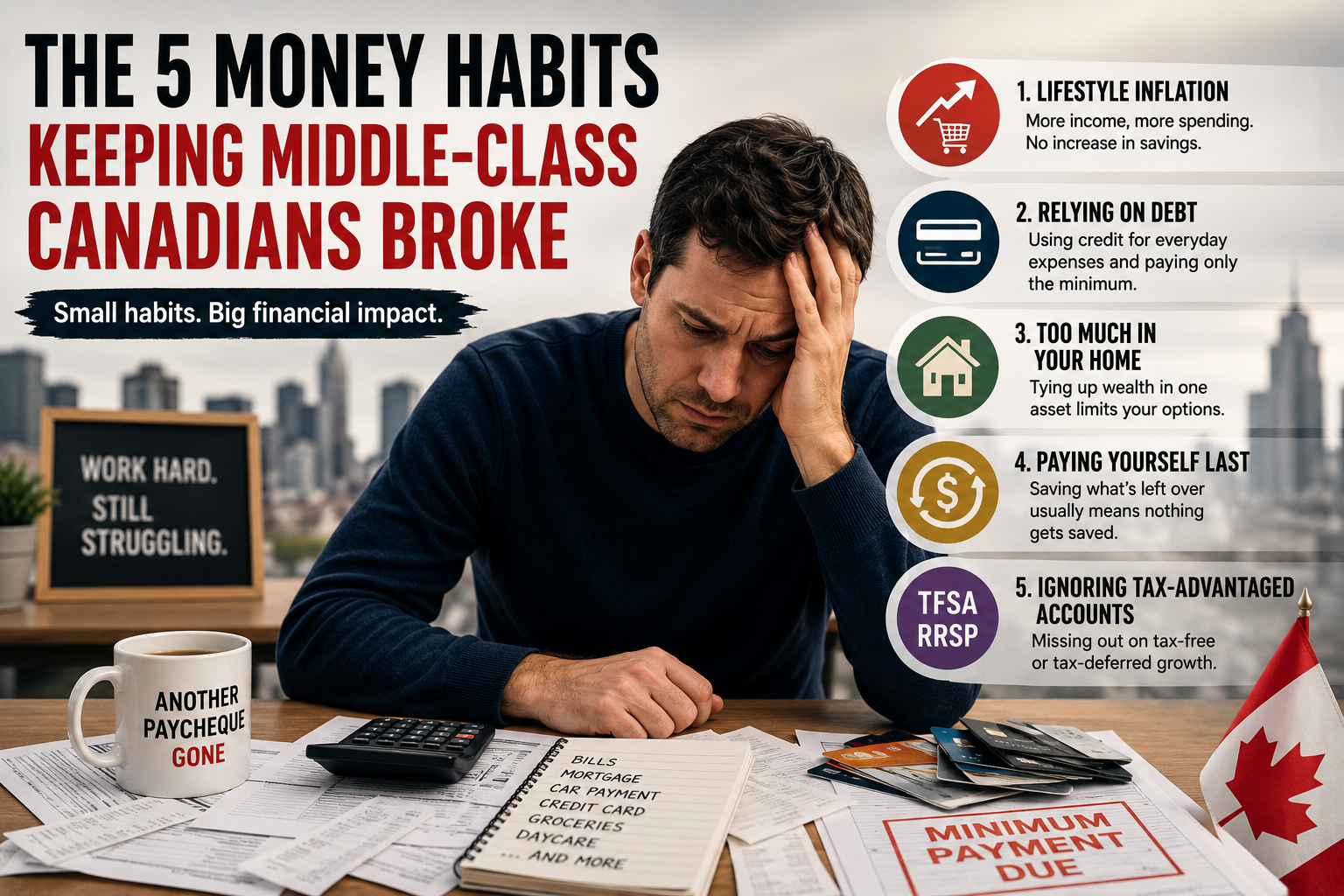

Why Higher Incomes Don't Always Create Financial Freedom

A larger paycheque does not automatically translate into a stronger financial position.

As income rises, many households immediately increase their spending. Bigger homes, newer vehicles, upgraded vacations, and additional monthly subscriptions often absorb most or all of the extra money coming in.

This pattern, commonly known as lifestyle inflation, can leave families living paycheque to paycheque despite earning substantially more than they did a few years earlier.

When fixed monthly expenses continually expand alongside income, financial flexibility becomes increasingly difficult to achieve.

How Debt Quietly Consumes Future Wealth

Debt is often treated as a normal part of everyday life.

Many Canadians regularly use credit cards for routine purchases such as groceries, fuel, and household expenses. While credit can be useful when managed carefully, problems emerge when balances are carried from month to month.

Several factors contribute to long-term debt challenges:

- Making only minimum monthly payments.

- Treating available credit as additional income.

- Carrying balances on multiple credit products.

- Paying interest for extended periods.

Minimum payments may seem manageable in the short term, but they can dramatically extend repayment timelines while directing significant amounts of money toward interest costs instead of savings or investments.

The Hidden Risk of Building Wealth Through One Asset

Homeownership remains an important financial goal for many Canadians.

However, problems can arise when a primary residence becomes the overwhelming center of a household's financial strategy.

A home typically comes with ongoing expenses that include:

- Mortgage payments.

- Property taxes.

- Maintenance costs.

- Insurance expenses.

When a large percentage of net worth is concentrated in a single property, households may have fewer opportunities to build diversified investments that offer liquidity and broader exposure to long-term growth.

Owning a home can be valuable, but relying on it as the sole path to wealth may limit financial flexibility.

The Cost of Waiting to Save What's Left Over

One of the most common wealth-building mistakes is saving only after all monthly spending is complete.

Unfortunately, there is often little money left at the end of the month.

Successful savers typically reverse this process by adopting a "pay yourself first" approach. Instead of waiting to see what remains, they automatically move money into savings and investment accounts immediately after receiving their pay.

This strategy can help support:

- Emergency funds.

- Retirement savings.

- Long-term investments.

- Future financial goals.

Automation removes much of the decision-making process and helps create consistency over time.

Why TFSA and RRSP Accounts Matter More Than Many Canadians Realize

Keeping savings in a standard account may feel safe, but it can reduce long-term growth potential.

Money held in low-interest accounts may struggle to keep pace with inflation, gradually reducing purchasing power over time.

Many Canadians also miss opportunities available through tax-advantaged accounts such as:

| Account | Key Benefit |

|---|---|

| TFSA | Tax-free investment growth |

| RRSP | Tax-deferred retirement savings |

These accounts can help investors retain more of their returns and potentially accelerate wealth accumulation compared with relying solely on traditional savings accounts.

Ignoring these tools may result in years of missed growth opportunities.

The Common Thread Behind These Financial Mistakes

Although these habits appear different on the surface, they share a common outcome: they reduce the amount of money available for long-term wealth creation.

Lifestyle inflation increases expenses. Debt redirects cash flow toward interest. Overreliance on housing concentrates risk. Delayed saving limits investment growth. Ignoring tax-advantaged accounts reduces the efficiency of wealth building.

Individually, each habit may seem manageable. Together, they can significantly slow financial progress over decades.

What Canadians Should Watch Going Forward

Financial success is rarely determined by a single investment or a single pay raise.

More often, it is the result of consistent habits repeated over many years. Small adjustments to spending, saving, debt management, and investing can compound into meaningful financial improvements over time.

For many households, identifying and correcting these five habits may be one of the most effective steps toward greater financial security.

FAQ: Brief Insights on Money Habits and Wealth Building

Why do higher earners still struggle financially?

Higher incomes often lead to higher spending. If expenses rise alongside earnings, little additional money is available for saving or investing.

Is paying only the minimum on a credit card a problem?

Yes. Minimum payments can keep debt outstanding for years and significantly increase total interest costs.

Is a home considered an investment?

A home can contribute to net worth, but relying entirely on one property for wealth creation can limit diversification and liquidity.

What does "pay yourself first" mean?

It means automatically directing money into savings or investments before spending on discretionary expenses.

Why are TFSA and RRSP accounts important?

They provide tax advantages that can help savings and investments grow more efficiently over the long term.