CPP vs OAS in Canada: Key Differences, Eligibility, Benefits and GIS Explained (2026)

Understanding retirement benefits can feel overwhelming, especially because many Canadians mistakenly assume that the Canada Pension Plan (CPP) and Old Age Security (OAS) are the same program.

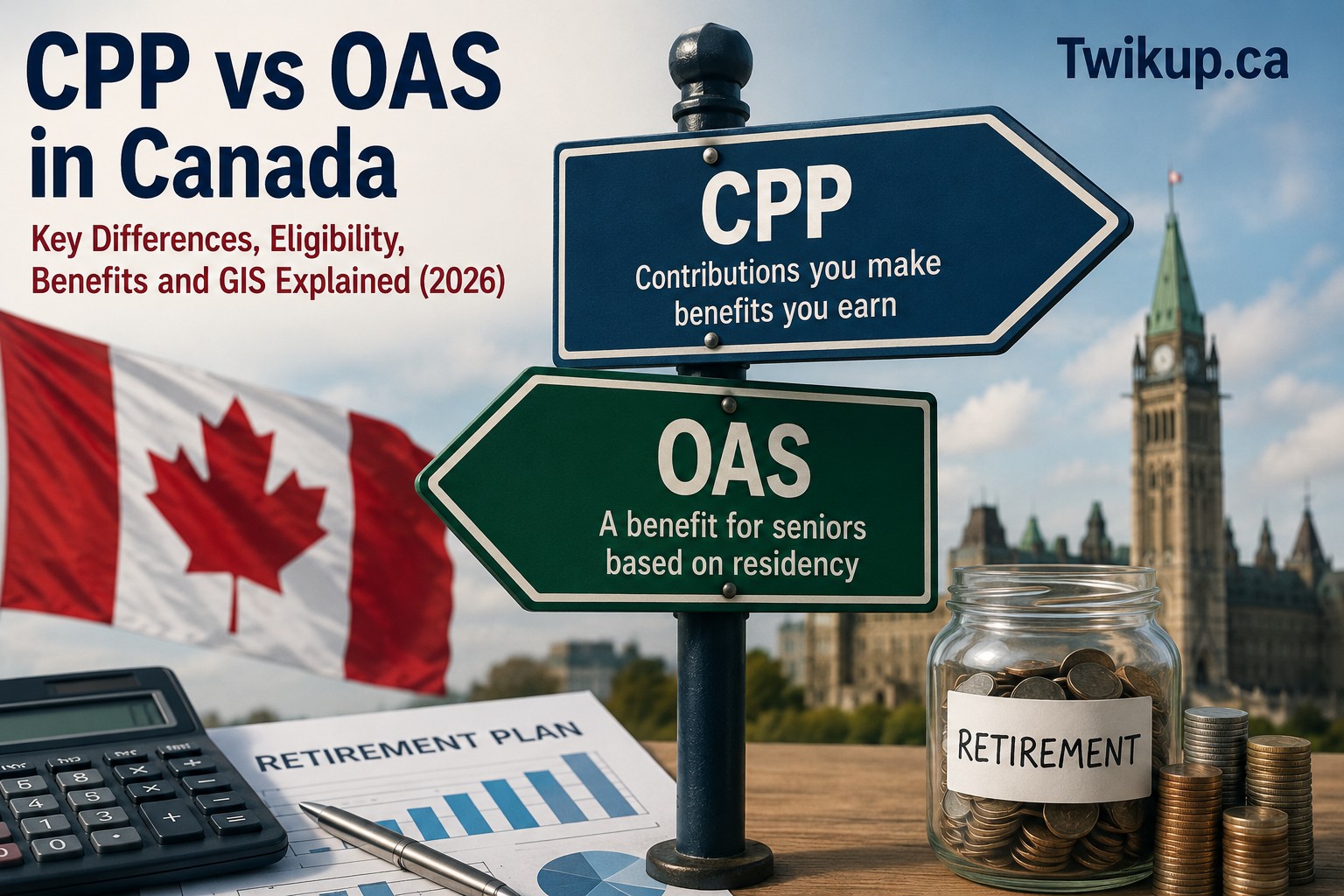

Although both provide income support to older Canadians, they operate very differently.

Understanding how these programs work can help Canadians prepare for retirement and make better financial decisions in 2026.

What Is the Canada Pension Plan (CPP)?

The Canada Pension Plan is a contributory public pension program.

Workers contribute to CPP during their working years through payroll deductions, and those contributions help determine future benefits.

Most employed and self-employed Canadians contribute to CPP.

The amount you receive depends on:

- How long you contributed.

- How much you earned during your working years.

- The age at which you begin receiving benefits.

CPP is designed to replace a portion of employment income after retirement and serves as one of the primary pillars of Canada's retirement system.

What Is Old Age Security (OAS)?

Old Age Security differs from CPP because it is not based on employment contributions.

Instead, OAS is funded through general tax revenues.

Eligibility depends primarily on:

- Age.

- Residency in Canada.

- Legal status.

Most Canadians become eligible for OAS at age 65.

Unlike CPP, OAS is intended to provide a basic level of retirement income regardless of an individual's work history.

Key Differences Between CPP and OAS

| Feature | CPP | OAS |

|---|---|---|

| Based on contributions | Yes | No |

| Funded by payroll contributions | Yes | No |

| Funded by taxes | No | Yes |

| Age of eligibility | 60–70 | 65+ |

| Depends on work history | Yes | No |

| Residency requirement | Limited | Important |

Although both programs support retirees, they serve different purposes and often work together as part of a broader retirement income strategy.

When Can You Start CPP?

Canadians may begin receiving CPP as early as age 60.

However, taking benefits early generally reduces monthly payments.

Waiting beyond age 65 increases benefits.

Many individuals choose to delay CPP to maximize retirement income.

For some retirees, delaying CPP can result in significantly higher lifetime benefits, particularly if they expect to live well into their 80s or beyond.

When Can You Start OAS?

Most Canadians become eligible at age 65.

Unlike CPP, OAS does not depend on employment contributions.

The amount received depends largely on residency requirements.

Canadians may also choose to delay OAS beyond age 65, which can increase monthly benefit amounts.

How Much Can Canadians Receive?

Payment amounts are adjusted periodically and depend on individual circumstances.

Factors influencing benefits include:

- Contribution history.

- Age.

- Years of Canadian residence.

- Income levels.

As of 2026, maximum CPP retirement benefits can exceed $1,400 per month for individuals who contributed at high levels throughout their careers. Actual payments are often lower because many Canadians do not contribute at the maximum level for their entire working lives.

OAS payments vary based on age and eligibility requirements, with most eligible seniors receiving monthly benefits that are adjusted quarterly to reflect inflation.

Because benefit levels change over time, Canadians should consult official government resources for the most current payment information.

What Is the OAS Clawback?

The Old Age Security recovery tax, commonly known as the OAS clawback, applies when annual income exceeds certain thresholds.

Higher-income seniors may have some or all of their OAS benefits reduced.

The clawback is based on net income reported on annual tax returns.

As retirement income rises, Canadians may see a portion of their OAS benefits recovered through the tax system.

What Is the Guaranteed Income Supplement (GIS)?

Low-income seniors receiving OAS may also qualify for the Guaranteed Income Supplement.

GIS provides additional financial assistance and is designed to support vulnerable seniors.

Unlike CPP, GIS is income-tested.

For many lower-income retirees, GIS can represent a significant source of monthly income and help offset rising living costs.

Can Immigrants Receive CPP and OAS?

Yes.

Permanent residents and immigrants may qualify, although eligibility rules differ.

CPP eligibility depends largely on contributions made while working in Canada.

OAS eligibility depends heavily on residency requirements.

International social security agreements may also affect eligibility for individuals who have lived or worked in multiple countries.

Can CPP and OAS Be Enough for Retirement?

For some Canadians, CPP and OAS may provide a meaningful portion of retirement income.

However, many retirees rely on multiple income sources, including:

- Workplace pensions.

- RRSPs.

- TFSAs.

- Personal investments.

- Rental income.

- Other savings.

Housing costs, inflation, healthcare expenses, and lifestyle goals all influence how much retirement income is needed.

Financial experts generally encourage Canadians to view CPP and OAS as foundational retirement benefits rather than complete retirement plans.

Should You Take CPP Early?

There is no universal answer.

Several factors influence this decision:

- Health.

- Life expectancy.

- Employment status.

- Savings.

- Retirement goals.

Some retirees prioritize immediate income, while others choose to maximize benefits by delaying payments.

The right decision depends on individual financial circumstances and long-term retirement objectives.

The Bigger Picture

CPP and OAS form the foundation of retirement income for millions of Canadians.

However, retirement planning extends beyond government benefits alone.

As Canadians face rising living costs, longer life expectancies, and evolving economic conditions, understanding how CPP, OAS, GIS, workplace pensions, and personal savings work together has become increasingly important.

A well-rounded retirement strategy can help provide greater financial security and flexibility throughout retirement.

Common Misconceptions

CPP and OAS Are the Same Program

False.

They are separate programs with different rules, funding mechanisms, and eligibility requirements.

Everyone Receives Maximum Benefits

False.

Benefits vary depending on contribution history, income, and residency history.

You Must Retire to Receive CPP

False.

Many Canadians continue working while collecting CPP.

OAS Depends on Employment Contributions

False.

OAS is based primarily on age and residency.

Frequently Asked Questions

Can I receive both CPP and OAS?

Yes.

Many retirees receive both programs simultaneously.

Can I collect CPP before age 65?

Yes.

Benefits may begin as early as age 60, although monthly payments are generally reduced.

Is OAS based on employment history?

No.

It primarily depends on residency requirements.

What is the GIS?

The Guaranteed Income Supplement provides additional support to low-income seniors who qualify for OAS.

Can immigrants qualify?

Yes.

Eligibility depends on contribution history and residency requirements.

Does CPP affect OAS?

No.

Receiving CPP does not automatically reduce OAS eligibility. However, higher total retirement income may contribute to the OAS clawback.

Can I work while receiving CPP?

Yes.

Many Canadians continue working while collecting CPP benefits.

Can I delay OAS?

Yes.

Delaying OAS beyond age 65 can increase monthly benefit payments.

Is CPP taxable?

Yes.

CPP benefits are generally considered taxable income and must be reported on annual tax returns.

Related Perspectives

Understanding retirement income is only one part of the broader financial picture facing Canadians. Rising living costs, healthcare concerns, economic uncertainty, and changing household finances all influence retirement planning.

-

What a Technical Recession Means for Canada as GDP Contracts for Two Straight Quarters

-

Canadians Are Saving Less: What It Means for Household Finances

Together, these articles provide additional context on how economic trends, health challenges, and personal finance decisions are shaping life in Canada in 2026.